A personal loan can be a lifesaver in times of urgent basis of financial need. Whether you’re planning a wedding, renovating your home, or covering tuition fees for your child in a boarding school, a personal loan can provide the necessary funds, especially when your finances are stretched. In such situations and more, securing a personal loan can be a practical solution.

Personal Loan Rate Interest

A personal loan doesn’t require any collateral, which is why the rate of interest are usually higher. Banks generally charge between 11% to 18% per year on personal loans.

Have you ever noticed how even a small change in interest rates can significantly lower your EMI?

Here, we’ll show you how just a 1% difference in personal loan interest can greatly reduce your monthly payments.

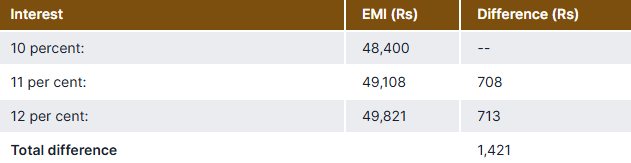

Imagine, (in case of personal loan rate interest), you take a personal loan of ₹15 lakh with a repayment period of three years. One bank offers an interest rate of 10%, another charges 11%, and a third one sets it at 12%.

Here’s how your monthly EMI would look in these cases:

- At a 10% interest rate, your EMI will be ₹48,400.

- If the rate increases to 11%, your EMI will rise to ₹49,108.

And if the interest rate rises to 12%, your EMI will go up further to ₹49,821.

In other words:

- At 11% interest, your EMI increases by ₹708.

- At 12% interest, your EMI jumps by a total of ₹1,421.

As shown in the table above, even a small increase in interest rates can make a noticeable difference in your monthly payments.

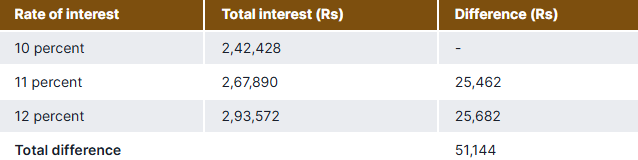

When the interest rate increases from 10% to 12%, the total interest you pay could go up by as much as ₹51,144. If the rate rises to 11%, your total interest would increase by ₹25,462.

To put it simply, with a 12% interest rate, your total interest liability would rise to ₹2.93 lakh, compared to ₹2.42 lakh at 10%.

So, it’s important to shop around for the best personal loan offer to minimize your interest payments.